SSA-89 Verification for Lenders: What You Need to Know

In today’s lending environment, identity fraud remains one of the biggest challenges facing financial institutions. As fraud tactics become increasingly sophisticated, lenders need reliable solutions to verify borrower identities quickly, securely, and compliantly. SSA-89 Verification for Lenders has become one of the most trusted methods for confirming borrower identity and reducing fraud risk during the loan approval process.

Understanding how SSA-89 verification works can help lenders reduce risk, strengthen compliance efforts, and improve confidence during the loan approval process.

What Is an SSA-89 Form?

The SSA-89 authorization form is issued by the Social Security Administration (SSA). It allows a lender or authorized third party to verify that a borrower’s name, Social Security number, and date of birth match SSA records.

This verification helps confirm that the borrower is who they claim to be, reducing the risk of identity fraud and synthetic identity schemes.

Unlike simply collecting a Social Security number, SSA-89 verification provides direct confirmation from the SSA database, making it one of the most reliable identity verification methods available to lenders.

Benefits of SSA-89 Verification for Lenders

Identity verification is a critical part of responsible lending. Fraudulent applications can lead to financial losses, compliance violations, delayed closings, and reputational damage.

SSA-89 verification helps lenders:

- Confirm borrower identity with greater confidence

- Detect inconsistencies early in the application process

- Reduce exposure to identity theft and fraud

- Support compliance with Know Your Customer (KYC) and anti-fraud requirements

- Improve underwriting accuracy

- Protect loan portfolios from unnecessary risk

For mortgage lenders especially, SSA-89 verification has become an important layer of protection in high-value transactions.

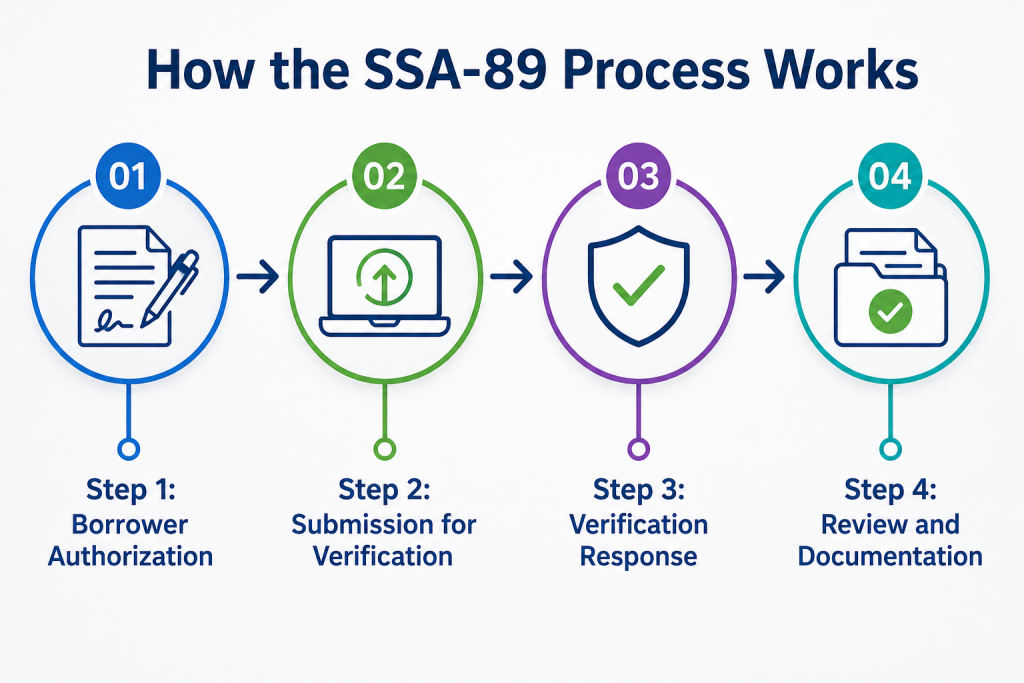

How the SSA-89 Process Works

The process is straightforward but must be handled carefully to ensure compliance.

Step 1: Borrower Authorization

The borrower completes and signs the SSA-89 form, granting permission for identity verification.

Step 2: Submission for Verification

The lender or authorized verification provider submits the information to the SSA for matching.

Step 3: Verification Response

The SSA confirms whether the submitted information matches its records.

Step 4: Review and Documentation

The lender reviews the results as part of the underwriting and fraud prevention process.

Because timing matters in lending, many lenders work with experienced verification providers who can streamline the process and help avoid delays.

Common Reasons Lenders Use SSA-89 Verification

Lenders often use SSA-89 verification for:

- Mortgage applications

- Home equity loans

- Refinancing transactions

- Commercial lending

- Consumer loans

- Fraud prevention reviews

- Suspicious or high-risk applications

It can also be valuable when documentation discrepancies appear during underwriting.

The Risks of Skipping Identity Verification

Failing to properly verify borrower identity can expose lenders to serious risks, including:

- Loan fraud losses

- Regulatory scrutiny

- Delayed funding

- Repurchase demands

- Increased default risk

- Damage to institutional reputation

As fraud schemes continue evolving, relying solely on basic documentation may no longer provide enough protection.

Choosing the Right Verification Partner

Not all verification providers offer the same level of accuracy, speed, or compliance expertise. When selecting a partner, lenders should look for:

- Industry experience

- Secure data handling practices

- Fast turnaround times

- Compliance knowledge

- Reliable customer support

- Transparent processes

Working with an experienced verification company like Private Eyes can help lenders streamline the verification process, strengthen fraud prevention efforts, and improve operational efficiency while maintaining compliance standards.

Key Takeaways

- SSA-89 verification allows lenders to confirm a borrower’s identity directly through Social Security Administration records.

- This process helps reduce identity fraud, synthetic identity fraud, and application inconsistencies.

- Accurate identity verification supports stronger underwriting decisions and protects loan portfolios.

- SSA-89 verification can help lenders meet compliance and fraud prevention requirements.

- Using a trusted verification partner can improve turnaround times, accuracy, and operational efficiency.

- Proactive identity verification helps lenders reduce financial risk and build greater confidence throughout the lending process.

Have questions? Speak to a Private Eyes expert for more information.