Identity Fraud Detection: 5 Red Flags That May Signal Borrower Identity Fraud

In today’s lending environment, fraudsters are becoming increasingly sophisticated in their attempts to secure loans using stolen or fabricated identities. Effective identity fraud detection is critical for lenders looking to reduce risk, protect assets, and maintain regulatory compliance. Recognizing the warning signs early can help prevent costly losses and protect both institutions and legitimate borrowers.

Here are five red flags that may indicate borrower identity fraud and why a robust identity fraud detection process is essential.

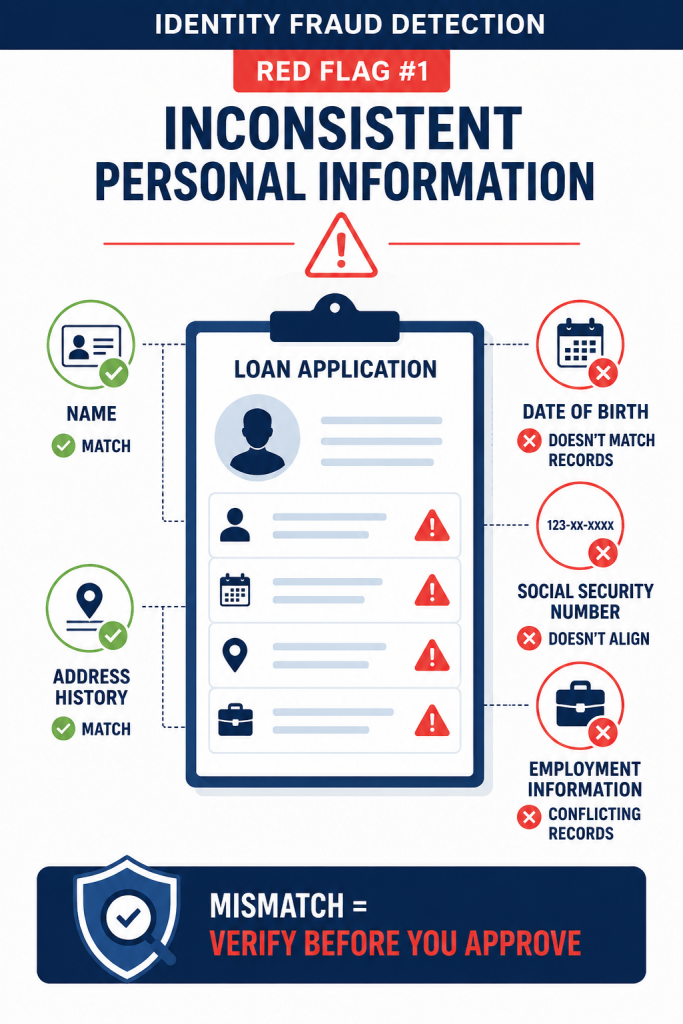

1. Inconsistent Personal Information

One of the most common indicators uncovered during identity fraud detection is conflicting personal information. A borrower’s application may contain discrepancies between their name, date of birth, Social Security number, address history, or employment details.

For example, if the Social Security number provided does not align with the applicant’s age or reported address history, further investigation is warranted. Cross-referencing information through trusted verification sources can help identify potential fraud before a loan is approved.

2. Recently Established Credit History

While some legitimate borrowers have limited credit histories, a newly established credit profile can sometimes be a warning sign. Fraudsters often create synthetic identities by combining real and fabricated information to build a credit history over time.

Identity fraud detection procedures should include reviewing the age of credit accounts, examining unusual credit-building patterns, and verifying the applicant’s identity through multiple independent sources.

3. Suspicious Documentation

Fraudulent borrowers may submit altered pay stubs, fake bank statements, counterfeit identification documents, or manipulated tax records. Advances in technology have made document forgery easier than ever.

Lenders should implement identity fraud detection tools that verify document authenticity and compare submitted information against reliable third-party databases. IRS transcript verification, employment verification, and income verification services can provide additional layers of protection.

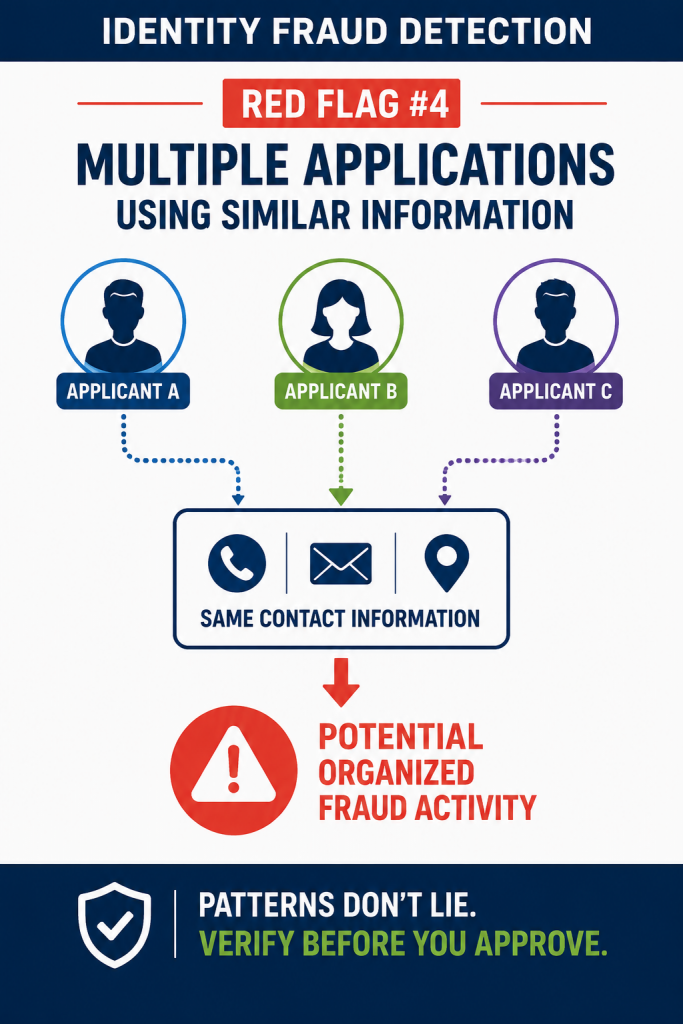

4. Multiple Applications Using Similar Information

A strong identity fraud detection program monitors for patterns across multiple applications. Fraudsters often reuse addresses, phone numbers, email accounts, or other identifying details across different loan applications.

If the same contact information appears repeatedly under different names or Social Security numbers, it may signal organized fraud activity. Automated fraud detection systems can quickly identify these patterns and flag applications for further review.

5. Difficulty Verifying Identity Through Trusted Sources

When an applicant’s identity cannot be verified through established verification methods, lenders should proceed with caution. Inability to validate Social Security information, employment history, income records, or government-issued identification may indicate identity fraud.

Services such as SSA-89 authorization processing, identity verification databases, and IRS transcript verification provide lenders with reliable tools for confirming applicant information. These safeguards strengthen identity fraud detection efforts and help prevent fraudulent loans from being funded.

Strengthening Your Identity Fraud Detection Strategy

Identity fraud continues to evolve, making proactive verification more important than ever. Financial institutions that invest in comprehensive identity fraud detection measures can reduce losses, improve compliance, and make more confident lending decisions.

By paying attention to these five warning signs and incorporating trusted verification tools into your workflow, your organization can identify potential fraud early and protect both your business and your customers.

When it comes to lending, effective identity fraud detection isn’t just about preventing losses; it’s about building trust and ensuring every decision is backed by verified information.

At Private Eyes, we help lenders strengthen their verification processes with identity verification, income verification, employment verification, and fraud prevention solutions designed to support faster, more confident decisions. To learn more about available verification tools and services, explore our solutions and discover how a stronger identity fraud detection strategy can help protect your organization.

Key Takeaways

- Identity fraud is a growing threat that can result in significant financial losses for lenders.

- Inconsistent personal information is often one of the earliest indicators of potential borrower fraud.

- Recently established credit histories may signal synthetic identity fraud and require additional scrutiny.

- Suspicious or altered documentation should always be verified through trusted third-party sources.

- Repeated use of the same contact information across multiple applications can indicate organized fraud activity.

- Identity verification tools such as SSA-89 processing, IRS transcript verification, and employment verification help strengthen fraud prevention efforts.

- A proactive identity fraud detection strategy helps lenders make informed decisions, reduce risk, and maintain compliance.

Have questions? Speak to a Private Eyes expert for more information.